Picture yourself scrolling through mortgage job boards at 11 PM, wondering if your resume truly captures those years spent building relationships with real estate agents, navigating rate sheets, and guiding anxious first-time homebuyers through the biggest purchase of their lives.

You've mastered the art of explaining debt-to-income ratios without making people's eyes glaze over, you've celebrated with families at closing tables, and you've probably lost count of how many times you've explained why a pre-approval isn't the same as a pre-qualification. Now you need a resume that tells that story - one that speaks fluently in both production metrics and human connection.

As a Mortgage Loan Officer, you occupy a unique position in the financial services world. You're not quite a banker, not exactly a salesperson, but rather a trusted advisor who translates complex financial regulations into accessible pathways toward homeownership. Whether you're coming from retail banking where you've been referring customers to the mortgage department for years, transitioning from real estate where you've seen deals fall apart due to financing issues, or climbing from loan processing where you've mastered the technical side but are ready for client interaction - your resume needs to demonstrate this distinctive blend of technical knowledge, sales acumen, and regulatory compliance that defines modern mortgage origination.

The mortgage industry has transformed dramatically since 2008, with the SAFE Act, TRID regulations, and constantly shifting market conditions creating a landscape where only the most adaptable and knowledgeable loan officers thrive. Your resume isn't just competing against other candidates - it's proving you can generate volume while maintaining pristine compliance records, build sustainable referral networks while interest rates fluctuate wildly, and guide borrowers through increasingly complex qualification requirements while keeping their trust and confidence intact.

In this comprehensive guide, we'll walk you through crafting a Mortgage Loan Officer resume that resonates with hiring managers who've seen it all. We'll start with selecting the right format - specifically why the reverse-chronological structure works best for showcasing your progression in financial services. Then we'll dive deep into structuring your work experience to highlight not just where you've worked, but the loan volume you've generated, the referral networks you've built, and the complex scenarios you've successfully navigated. We'll explore which skills actually matter in today's mortgage market, from specific loan origination systems to nuanced knowledge of FHA, VA, and conventional products. You'll learn how to present your education and licensing credentials prominently (because that NMLS number is non-negotiable), how to showcase awards and achievements that prove consistent performance across market cycles, and how to craft a cover letter that demonstrates your understanding of the delicate balance between sales targets and fiduciary responsibility.

We'll also address the specific considerations that set mortgage resumes apart - like how to subtly communicate your compliance track record, ways to demonstrate local market knowledge that takes years to develop, and strategies for highlighting your referral source development when sustainable success depends more on relationships than cold calling. Whether you're licensed in multiple states, specializing in first-time homebuyers, or transitioning from processing to origination, we'll cover the nuances that make your situation unique. By the end, you'll have everything needed to create a resume that doesn't just list your experience, but tells the story of a loan officer who generates volume while maintaining compliance, who builds lasting professional relationships, and who guides borrowers through one of life's most significant financial decisions.

The reverse-chronological format is your best friend here. Why? Because hiring managers at mortgage companies and banks want to see your progression in the financial services industry immediately. They're looking for patterns - did you start in customer service and work your way up? Have you been consistently hitting sales targets?

The reverse-chronological format puts your most recent (and likely most relevant) experience front and center.

Start with a professional summary that speaks directly to your ability to originate loans, build referral networks, and navigate complex regulations. This isn't the place for generic statements about being a "team player."

Instead, think about what makes you stand out in the mortgage industry specifically.

❌ Don't write a vague summary:

Experienced professional seeking Mortgage Loan Officer position.

Strong communication skills and attention to detail.

✅ Do write a targeted summary:

Licensed Mortgage Loan Officer with 3+ years originating $12M+ in residential loans annually.

Expert in FHA, VA, and conventional loan products with proven ability to build referral

partnerships with 20+ real estate agents. NMLS #123456.

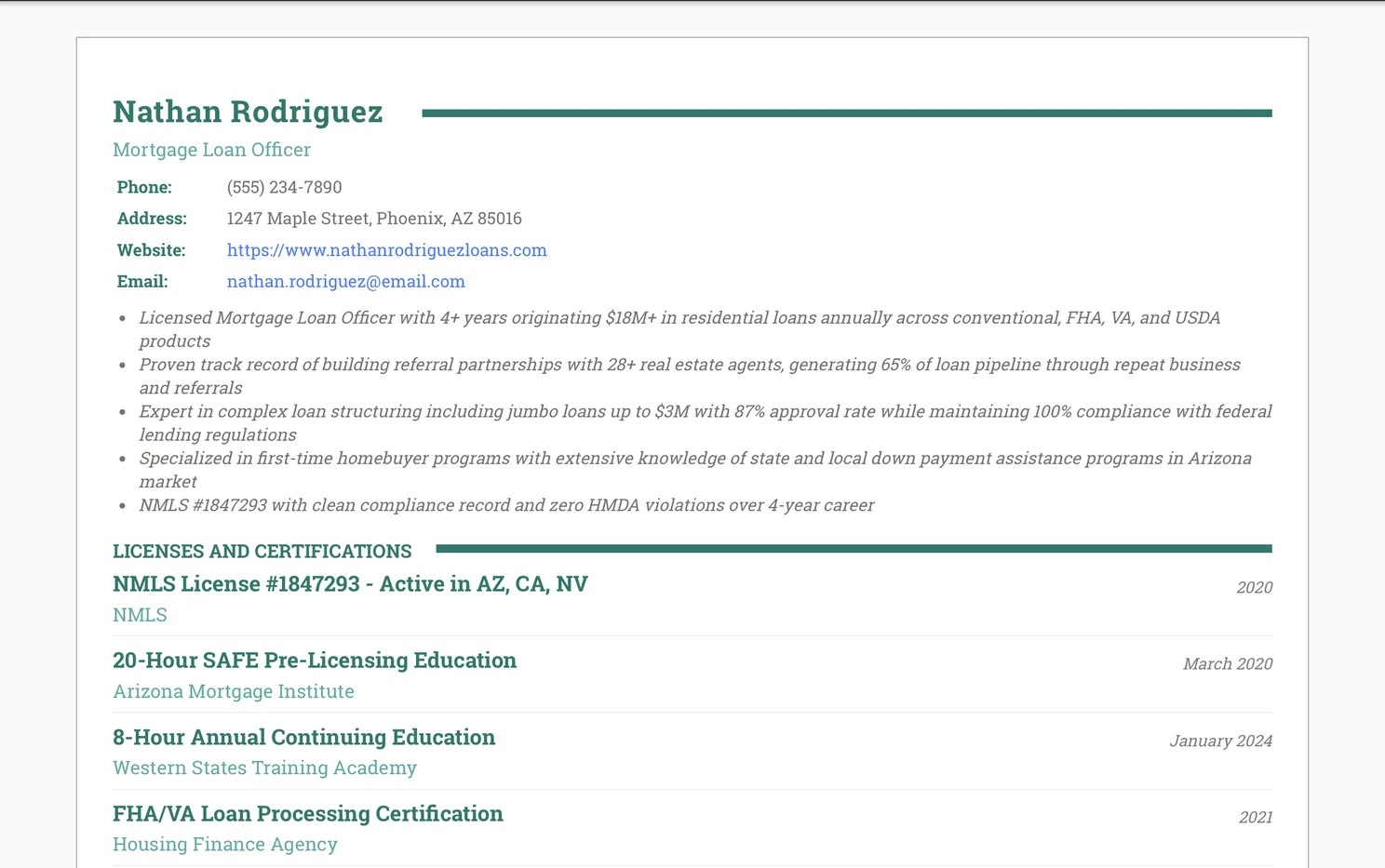

After your summary, organize your resume with these critical sections - Contact Information (including your NMLS number prominently), Professional Summary, Licenses and Certifications, Work Experience, Skills, and Education.

The placement of your licenses section is crucial - if you're already licensed, put it high up on the page, right after your summary. If you're still pursuing your NMLS license, you can include it in a "Certifications in Progress" section.

Remember that mortgage lending is heavily regulated across all markets. In the USA, your NMLS number is non-negotiable. In Canada, you'll need to highlight your provincial licensing. UK readers should emphasize their CeMAP qualification, while Australian applicants need to showcase their Certificate IV in Finance and Mortgage Broking.

Your work experience section is where you transform from a name on paper to a revenue-generating professional.

Hiring managers aren't just looking at where you worked - they're calculating your potential contribution to their loan volume. They want to see numbers, loan types, and evidence of your ability to navigate the complex dance between borrowers, underwriters, and real estate professionals.

Every bullet point in your work experience should tell a story of success. Start with strong action verbs that reflect the core activities of mortgage origination - originated, structured, cultivated, converted. Then add the numbers that prove your impact. How many loans did you close? What was your total loan volume?

What was your application-to-close ratio?

❌ Don't write generic job descriptions:

Mortgage Loan Officer - ABC Bank (2021-2023)

• Helped customers with mortgage applications

• Worked with real estate agents

• Processed loan documents

• Met sales goals

✅ Do write achievement-focused bullets:

Mortgage Loan Officer - ABC Bank (2021-2023)

• Originated average of $1.5M monthly in residential mortgages, exceeding targets by 25%

• Cultivated referral network of 22 real estate agents, generating 60% of loan pipeline

• Structured complex loan scenarios including jumbo loans up to $2M with 85% approval rate

• Reduced average loan processing time from 45 to 32 days through proactive communication

Managing multiple loans simultaneously while maintaining compliance standards is an art form unique to this role.

Your experience section should reflect your ability to juggle numerous applications at various stages. Include metrics about your pipeline size, conversion rates, and how you've improved processes.

If you're transitioning from a related role like loan processor or personal banker, frame your experience through the lens of loan origination. That time you helped customers understand loan products as a bank teller? That's "Educated 50+ customers monthly on mortgage products, identifying qualified leads for loan officers." Your experience processing loans? That becomes "Processed 200+ mortgage applications with 98% accuracy, gaining deep knowledge of underwriting requirements."

The best Mortgage Loan Officers know that success comes from relationships, not cold calls. Your work experience should demonstrate your ability to build and maintain professional networks.

Include specific examples of partnerships you've developed, community involvement that generated business, or creative marketing initiatives you've implemented.

Here's the reality - every Mortgage Loan Officer resume will claim "excellent communication skills" and "attention to detail." But the hiring manager reading your resume has seen those phrases a thousand times.

What they're really looking for are the specific competencies that separate successful loan officers from those who struggle to build a sustainable pipeline.

Start with the software and systems that power the mortgage industry.

Encompass360, Calyx Point, or whatever loan origination system you've mastered should be listed specifically. Don't just say "LOS experience" - name the actual platforms. Include your proficiency with automated underwriting systems like Desktop Underwriter (DU) and Loan Product Advisor (LPA). These technical skills show you can hit the ground running.

❌ Don't list vague technical skills:

• Computer proficient

• Mortgage software

• Microsoft Office

✅ Do list specific industry tools:

• Encompass360 and Calyx Point loan origination systems

• Desktop Underwriter (DU) and LP automated underwriting

• Optimal Blue pricing engine

• Salesforce CRM for pipeline management

Your skills section should reflect your understanding of the complex regulatory environment. List specific regulations you're well-versed in - TRID, RESPA, Fair Lending practices. Then showcase your product knowledge. Can you originate FHA loans with down payment assistance? Are you experienced with VA loans including the specific requirements for Certificate of Eligibility? Do you understand the nuances of jumbo loans versus conforming loans?

This specificity demonstrates expertise that generic skills never could.

Yes, you need to include sales-related skills, but make them specific to mortgage lending. Instead of "sales skills," write "consultative selling for complex financial products." Rather than "networking," specify "referral partner development with real estate professionals." Transform "customer service" into "borrower education on loan programs and qualification requirements."

These contextualized skills show you understand that selling mortgages isn't like selling retail products - it requires education, trust-building, and long-term relationship management.

Now let's talk about what makes a Mortgage Loan Officer resume truly stand out from the stack.

You're competing against other candidates who also have NMLS licenses, who also know loan products, who also claim strong sales skills. The difference-makers are in the details that show you understand the unique challenges and opportunities of this role.

Every hiring manager's nightmare is bringing on a loan officer who generates compliance violations.

Your resume should subtly but clearly communicate that you're not that person. Weave compliance awareness throughout your resume - mention your clean NMLS record, highlight any compliance training you've completed, and when describing achievements, include phrases like "while maintaining 100% compliance with federal lending regulations."

If you've never had a loan kicked back for compliance issues, that's worth mentioning.

❌ Don't ignore compliance considerations:

Originated high volume of loans with strong sales performance

✅ Do integrate compliance awareness:

Originated $18M in loans annually while maintaining perfect compliance record

with zero HMDA violations or fair lending concerns over 3-year period

Mortgage lending is inherently local, even when working for national lenders. Demonstrate your understanding of your specific market - mention your knowledge of local down payment assistance programs, your relationships with regional real estate brokerages, or your expertise with unique aspects of your market (like co-ops in New York, or agricultural properties in rural areas).

This shows you bring more than just general lending knowledge - you bring local market intelligence that takes years to develop.

Unlike many sales roles where leads come from marketing or cold outreach, successful Mortgage Loan Officers build their business through referral partnerships. Your resume should tell the story of how you develop and maintain these crucial relationships. Include specific examples - "Established preferred lender status with three top-producing real estate teams" or "Created monthly first-time homebuyer workshops that generated 25% of annual loan volume."

These specifics show you understand that sustainable success in mortgage lending comes from being a trusted advisor, not just a salesperson.

The mortgage industry is experiencing rapid technological change, from digital applications to automated verification systems.

Show that you're not just comfortable with technology, but that you actively leverage it to improve the borrower experience. Mention your use of digital tools like mobile loan applications, e-signatures, or video consultations. If you've maintained strong production during the shift to remote work, that's particularly relevant. This demonstrates adaptability that's crucial in today's evolving mortgage landscape.

Remember, your resume is often your first interaction with a potential employer in an industry built on trust and relationships. Every element should reinforce that you're not just qualified on paper, but that you understand the nuanced realities of originating mortgages in today's complex lending environment.

The goal isn't just to list your experience - it's to tell the story of a loan officer who generates volume while maintaining compliance, who builds lasting professional relationships, and who guides borrowers through one of the biggest financial decisions of their lives.

The mortgage industry has evolved significantly since the 2008 financial crisis, with stricter regulations like the SAFE Act requiring specific educational credentials. Your education section isn't just a formality - it's proof that you're legally qualified to originate loans and that you possess the foundational knowledge to navigate an increasingly complex regulatory landscape.

For Mortgage Loan Officers, education extends beyond traditional degrees.

You'll need to showcase your NMLS (Nationwide Multistate Licensing System) education, which includes 20 hours of pre-licensing education covering federal law, ethics, and lending standards. This isn't optional - it's the ticket to your career. List these certifications prominently, including your NMLS number once obtained.

While a bachelor's degree isn't always mandatory, having one in finance, economics, business administration, or accounting gives you a competitive edge. Community banks might be flexible, but larger institutions often filter candidates without degrees.

The key is presenting your education in a way that demonstrates both compliance and competence.

Start with your highest level of formal education, then add your mortgage-specific certifications. Include completion dates for NMLS courses - this shows you're current with regulations.

If you're transitioning from real estate, banking, or insurance, highlight relevant coursework that translates to mortgage lending.

❌ Don't write vaguely about your qualifications:

Bachelor's Degree - State University

NMLS Licensed

Some mortgage training courses

✅ Do provide specific, compliance-focused details:

Bachelor of Science in Finance - State University, 2021

GPA: 3.6/4.0 | Relevant Coursework: Real Estate Finance, Risk Management, Financial Markets

NMLS License #1234567 - Active in CA, NV, AZ (2023)

• 20-Hour SAFE Pre-Licensing Education - ABC Training Institute (March 2023)

• 8-Hour Annual Continuing Education - XYZ Academy (January 2024)

• FHA/VA Loan Processing Certification - Housing Finance Agency (2023)

Different states have varying requirements beyond federal minimums. California requires additional education on state-specific laws, while Texas has unique homestead regulations you'll need to understand.

If you're licensed in multiple states, list them clearly - this versatility is valuable to employers operating across state lines.

The mortgage industry rewards continuous learning. Include any additional certifications like Certified Mortgage Planning Specialist (CMPS) or coursework in specialized areas like reverse mortgages or construction loans.

These show you're not just meeting minimum requirements but actively expanding your expertise to serve diverse client needs.

Unlike other sales roles where awards might focus purely on volume, mortgage lending recognition often balances production with quality metrics like customer satisfaction scores, loan quality ratings, and compliance excellence. Your awards section needs to reflect this multifaceted nature of success in mortgage origination.

Production awards are the most common - President's Club, Top Producer, Million Dollar Club - but context is everything. A "Top 10% Producer" award at Wells Fargo carries different weight than the same achievement at a local credit union.

Specify loan volume in dollars rather than just units, as this demonstrates your ability to handle complex, high-value transactions.

Quality and compliance awards are increasingly valuable post-Dodd-Frank. Recognition for lowest default rates, highest customer satisfaction scores, or perfect compliance audits shows you're not just closing loans - you're closing the right loans. These awards reassure employers that you won't create regulatory headaches while chasing numbers.

❌ Don't list awards without context:

Top Producer - 2023

Customer Service Award

Best Team Player

✅ Do provide specific, quantifiable achievements:

President's Club Award - ABC Mortgage Corporation (2023)

• Top 5% nationally with $42M in funded loans across 156 transactions

• Maintained 0% early payment default rate and 98% customer satisfaction score

Excellence in FHA Lending Award - Regional Housing Authority (2022)

• Recognized for helping 47 first-time homebuyers achieve homeownership

• Specialized in down payment assistance programs with 100% compliance rate

Publications in mortgage lending might include articles in industry journals like National Mortgage News or Mortgage Professional America, blog posts on company websites about market trends, or contributions to local real estate publications. These demonstrate your market expertise and ability to educate clients - crucial skills when explaining complex loan products.

If you've written guides on topics like "Navigating VA Loans" or "Understanding Debt-to-Income Ratios," include them. These show you can break down complex concepts for clients. Speaking engagements at real estate offices or first-time homebuyer seminars also belong here - they prove your role as a trusted advisor in your community.

Create a separate "Awards & Recognition" section if you have three or more significant achievements.

Otherwise, integrate them into your experience section where they provide context for your accomplishments. Recent awards (within three years) are most relevant, unless older awards are particularly prestigious or from well-known institutions.

Remember that in mortgage lending, consistency matters as much as peaks. An award for "Five Years Consecutive President's Club" tells a better story than a single spectacular year.

It shows you can maintain performance through different market cycles - a valuable trait given the mortgage industry's sensitivity to interest rate changes.

The mortgage industry's interconnected nature means your reputation travels fast.

A reference from a respected real estate broker can open doors at multiple lenders, while a negative reference can close them just as quickly. Your references aren't just confirming employment - they're vouching for your ability to handle people's largest financial transactions with integrity and competence.

Your ideal references understand what makes a successful Mortgage Loan Officer. A branch manager who can speak to your production numbers, pull-through rates, and compliance record provides more value than a generic "hard worker" recommendation. Processing managers can attest to your application quality and attention to detail.

Underwriters (if you have good relationships) can confirm your ability to structure deals correctly the first time.

Real estate agent references require careful consideration. Choose established agents who've sent you multiple referrals over time, not just someone from a single transaction. Their endorsement carries weight because it represents repeated trust with their clients' financing. Similarly, builder representatives or financial advisors who've referred business demonstrate your ability to maintain professional partnerships.

❌ Don't list references without context:

References:

John Smith - 555-1234

Jane Doe - 555-5678

Bob Johnson - 555-9012

✅ Do provide references with clear professional relationships:

Professional References:

Sarah Martinez - Regional Sales Manager, First National Mortgage

Phone: 555-1234 | Email: [email protected]

Relationship: Direct supervisor for 3 years; can attest to $150M production volume

and consistent President's Club achievement

Michael Chen - Managing Broker, Premier Realty Group

Phone: 555-5678 | Email: [email protected]

Relationship: Primary referral partner; 50+ successful transactions together;

can speak to client service and communication skills

Mortgage lending often involves non-compete agreements and client confidentiality issues that complicate references.

If you're currently employed, you might not want your manager contacted immediately. Create a separate reference sheet noting "References available upon request - currently employed and conducting confidential search." This is standard in the industry and won't raise red flags.

When listing references from previous employers, be mindful of any non-solicitation agreements. A former colleague now at a different company might be a safer reference than someone still at your previous firm if there are competitive concerns. Always inform your references about potential calls and brief them on the position you're seeking - they should know if you're moving from retail to wholesale or shifting to a different market segment.

Different markets have varying reference expectations.

In the UK, employers often require written references on company letterhead. Australian employers might check your credit as part of their reference process. In Canada, privacy laws affect what previous employers can disclose. In the USA, some states have specific regulations about what employers can say about former employees.

Include at least one reference who can verify your licensing status and continuing education compliance. This might be a compliance officer or training coordinator.

Given the regulatory scrutiny in mortgage lending, having someone who can confirm your clean compliance record is invaluable.

Keep your reference list updated quarterly - production numbers change, people change positions, and contact information becomes outdated. After each successful placement, update your references on your new role and thank them for their support.

This maintains relationships for future opportunities.

Create different reference lists for different opportunities. Applying to a reverse mortgage specialist position? Include references who can speak to your experience with senior clients. Pursuing a construction lending role? Builder and contractor references become more relevant. This targeted approach shows strategic thinking and network depth.

Finally, remember that in mortgage lending, your references often become your future business partners. The manager who gives you a glowing reference today might become your wholesale account executive tomorrow. Treat every professional relationship as a long-term investment in your career network.

The mortgage industry's relationship-driven nature makes cover letters particularly crucial. Hiring managers want to see that you understand the delicate balance between sales targets and fiduciary responsibility.

They're looking for someone who can build referral networks with real estate agents while maintaining compliance standards that protect both borrowers and the institution.

Skip the generic "I'm writing to apply" opening.

Instead, lead with a specific achievement that demonstrates your understanding of current market challenges. Maybe you maintained loan volume during rising rate environments by pivoting to ARM products, or you built a thriving first-time homebuyer practice using state bond programs. Your opening should immediately signal that you understand the mortgage business beyond just taking applications.

❌ Don't open with generic enthusiasm:

Dear Hiring Manager,

I am excited to apply for the Mortgage Loan Officer position at your company.

I have been working in sales for five years and think I would be a great fit.

✅ Do lead with specific, relevant achievements:

Dear Ms. Johnson,

When interest rates jumped to 7% last year, I helped 73 families still achieve

homeownership by leveraging creative financing solutions including 2-1 buydowns

and state housing finance programs - maintaining my $3M monthly production target

while competitors saw 40% volume drops.

The mortgage industry constantly evolves - from TRID implementation to COVID-era forbearance programs to recent NAR settlement changes affecting buyer representation. Use your cover letter to show you're not just aware of these changes but have successfully adapted to them.

Mention specific programs you've mastered like FHA 203(k) renovation loans or USDA rural development loans if they're relevant to the employer's market.

Address the employer's specific market position. If they're a direct lender, emphasize your ability to sell in-house products. If they're a broker, highlight your relationships with multiple wholesale lenders. For credit unions, stress your member-service philosophy. This customization shows you understand their business model, not just the generic role of loan origination.

Mortgage lending success depends heavily on referral partnerships.

Describe how you've built relationships with real estate agents, financial planners, or builders. But balance this with compliance awareness - mention your clean audit record or your commitment to fair lending practices. Post-2008, employers need to know you can produce without creating regulatory risk.

Include specific examples of complex scenarios you've navigated - perhaps helping self-employed borrowers document income or structuring loans for investment properties. These examples demonstrate problem-solving abilities that go beyond basic order-taking.

End with specificity about what you bring to their team. If they're expanding into reverse mortgages and you have HECM experience, mention it. If they're growing their Hispanic market presence and you're bilingual, emphasize this alignment. Propose a concrete next step beyond "I look forward to hearing from you."

Remember that in mortgage lending, timing matters. Mention your current pipeline status and potential transfer timeline if you're currently originating. This shows professionalism and helps set realistic expectations about your availability while respecting any non-compete agreements you might have.

After diving deep into the intricacies of crafting a compelling Mortgage Loan Officer resume, here are the essential points to remember as you build yours:

Creating a standout Mortgage Loan Officer resume doesn't have to be overwhelming. With Resumonk, you can build a professional, polished resume that incorporates all these crucial elements while maintaining clean, readable formatting that hiring managers expect. Our AI-powered suggestions help you craft achievement-focused bullet points that showcase your loan origination success, while our professionally designed templates ensure your NMLS credentials, production metrics, and compliance achievements are presented with the prominence they deserve. Whether you're transitioning from processing, moving between lenders, or advancing your career in mortgage origination, Resumonk's tools are specifically designed to help financial services professionals like you tell their story effectively.

Ready to create your standout Mortgage Loan Officer resume?

Join hundreds of mortgage professionals who've successfully advanced their careers with Resumonk's intelligent resume builder. Our specialized templates and industry-specific recommendations will help you craft a resume that speaks directly to hiring managers in the mortgage industry.

Start Building Your Mortgage Loan Officer Resume →

Picture yourself scrolling through mortgage job boards at 11 PM, wondering if your resume truly captures those years spent building relationships with real estate agents, navigating rate sheets, and guiding anxious first-time homebuyers through the biggest purchase of their lives.

You've mastered the art of explaining debt-to-income ratios without making people's eyes glaze over, you've celebrated with families at closing tables, and you've probably lost count of how many times you've explained why a pre-approval isn't the same as a pre-qualification. Now you need a resume that tells that story - one that speaks fluently in both production metrics and human connection.

As a Mortgage Loan Officer, you occupy a unique position in the financial services world. You're not quite a banker, not exactly a salesperson, but rather a trusted advisor who translates complex financial regulations into accessible pathways toward homeownership. Whether you're coming from retail banking where you've been referring customers to the mortgage department for years, transitioning from real estate where you've seen deals fall apart due to financing issues, or climbing from loan processing where you've mastered the technical side but are ready for client interaction - your resume needs to demonstrate this distinctive blend of technical knowledge, sales acumen, and regulatory compliance that defines modern mortgage origination.

The mortgage industry has transformed dramatically since 2008, with the SAFE Act, TRID regulations, and constantly shifting market conditions creating a landscape where only the most adaptable and knowledgeable loan officers thrive. Your resume isn't just competing against other candidates - it's proving you can generate volume while maintaining pristine compliance records, build sustainable referral networks while interest rates fluctuate wildly, and guide borrowers through increasingly complex qualification requirements while keeping their trust and confidence intact.

In this comprehensive guide, we'll walk you through crafting a Mortgage Loan Officer resume that resonates with hiring managers who've seen it all. We'll start with selecting the right format - specifically why the reverse-chronological structure works best for showcasing your progression in financial services. Then we'll dive deep into structuring your work experience to highlight not just where you've worked, but the loan volume you've generated, the referral networks you've built, and the complex scenarios you've successfully navigated. We'll explore which skills actually matter in today's mortgage market, from specific loan origination systems to nuanced knowledge of FHA, VA, and conventional products. You'll learn how to present your education and licensing credentials prominently (because that NMLS number is non-negotiable), how to showcase awards and achievements that prove consistent performance across market cycles, and how to craft a cover letter that demonstrates your understanding of the delicate balance between sales targets and fiduciary responsibility.

We'll also address the specific considerations that set mortgage resumes apart - like how to subtly communicate your compliance track record, ways to demonstrate local market knowledge that takes years to develop, and strategies for highlighting your referral source development when sustainable success depends more on relationships than cold calling. Whether you're licensed in multiple states, specializing in first-time homebuyers, or transitioning from processing to origination, we'll cover the nuances that make your situation unique. By the end, you'll have everything needed to create a resume that doesn't just list your experience, but tells the story of a loan officer who generates volume while maintaining compliance, who builds lasting professional relationships, and who guides borrowers through one of life's most significant financial decisions.

The reverse-chronological format is your best friend here. Why? Because hiring managers at mortgage companies and banks want to see your progression in the financial services industry immediately. They're looking for patterns - did you start in customer service and work your way up? Have you been consistently hitting sales targets?

The reverse-chronological format puts your most recent (and likely most relevant) experience front and center.

Start with a professional summary that speaks directly to your ability to originate loans, build referral networks, and navigate complex regulations. This isn't the place for generic statements about being a "team player."

Instead, think about what makes you stand out in the mortgage industry specifically.

❌ Don't write a vague summary:

Experienced professional seeking Mortgage Loan Officer position.

Strong communication skills and attention to detail.

✅ Do write a targeted summary:

Licensed Mortgage Loan Officer with 3+ years originating $12M+ in residential loans annually.

Expert in FHA, VA, and conventional loan products with proven ability to build referral

partnerships with 20+ real estate agents. NMLS #123456.

After your summary, organize your resume with these critical sections - Contact Information (including your NMLS number prominently), Professional Summary, Licenses and Certifications, Work Experience, Skills, and Education.

The placement of your licenses section is crucial - if you're already licensed, put it high up on the page, right after your summary. If you're still pursuing your NMLS license, you can include it in a "Certifications in Progress" section.

Remember that mortgage lending is heavily regulated across all markets. In the USA, your NMLS number is non-negotiable. In Canada, you'll need to highlight your provincial licensing. UK readers should emphasize their CeMAP qualification, while Australian applicants need to showcase their Certificate IV in Finance and Mortgage Broking.

Your work experience section is where you transform from a name on paper to a revenue-generating professional.

Hiring managers aren't just looking at where you worked - they're calculating your potential contribution to their loan volume. They want to see numbers, loan types, and evidence of your ability to navigate the complex dance between borrowers, underwriters, and real estate professionals.

Every bullet point in your work experience should tell a story of success. Start with strong action verbs that reflect the core activities of mortgage origination - originated, structured, cultivated, converted. Then add the numbers that prove your impact. How many loans did you close? What was your total loan volume?

What was your application-to-close ratio?

❌ Don't write generic job descriptions:

Mortgage Loan Officer - ABC Bank (2021-2023)

• Helped customers with mortgage applications

• Worked with real estate agents

• Processed loan documents

• Met sales goals

✅ Do write achievement-focused bullets:

Mortgage Loan Officer - ABC Bank (2021-2023)

• Originated average of $1.5M monthly in residential mortgages, exceeding targets by 25%

• Cultivated referral network of 22 real estate agents, generating 60% of loan pipeline

• Structured complex loan scenarios including jumbo loans up to $2M with 85% approval rate

• Reduced average loan processing time from 45 to 32 days through proactive communication

Managing multiple loans simultaneously while maintaining compliance standards is an art form unique to this role.

Your experience section should reflect your ability to juggle numerous applications at various stages. Include metrics about your pipeline size, conversion rates, and how you've improved processes.

If you're transitioning from a related role like loan processor or personal banker, frame your experience through the lens of loan origination. That time you helped customers understand loan products as a bank teller? That's "Educated 50+ customers monthly on mortgage products, identifying qualified leads for loan officers." Your experience processing loans? That becomes "Processed 200+ mortgage applications with 98% accuracy, gaining deep knowledge of underwriting requirements."

The best Mortgage Loan Officers know that success comes from relationships, not cold calls. Your work experience should demonstrate your ability to build and maintain professional networks.

Include specific examples of partnerships you've developed, community involvement that generated business, or creative marketing initiatives you've implemented.

Here's the reality - every Mortgage Loan Officer resume will claim "excellent communication skills" and "attention to detail." But the hiring manager reading your resume has seen those phrases a thousand times.

What they're really looking for are the specific competencies that separate successful loan officers from those who struggle to build a sustainable pipeline.

Start with the software and systems that power the mortgage industry.

Encompass360, Calyx Point, or whatever loan origination system you've mastered should be listed specifically. Don't just say "LOS experience" - name the actual platforms. Include your proficiency with automated underwriting systems like Desktop Underwriter (DU) and Loan Product Advisor (LPA). These technical skills show you can hit the ground running.

❌ Don't list vague technical skills:

• Computer proficient

• Mortgage software

• Microsoft Office

✅ Do list specific industry tools:

• Encompass360 and Calyx Point loan origination systems

• Desktop Underwriter (DU) and LP automated underwriting

• Optimal Blue pricing engine

• Salesforce CRM for pipeline management

Your skills section should reflect your understanding of the complex regulatory environment. List specific regulations you're well-versed in - TRID, RESPA, Fair Lending practices. Then showcase your product knowledge. Can you originate FHA loans with down payment assistance? Are you experienced with VA loans including the specific requirements for Certificate of Eligibility? Do you understand the nuances of jumbo loans versus conforming loans?

This specificity demonstrates expertise that generic skills never could.

Yes, you need to include sales-related skills, but make them specific to mortgage lending. Instead of "sales skills," write "consultative selling for complex financial products." Rather than "networking," specify "referral partner development with real estate professionals." Transform "customer service" into "borrower education on loan programs and qualification requirements."

These contextualized skills show you understand that selling mortgages isn't like selling retail products - it requires education, trust-building, and long-term relationship management.

Now let's talk about what makes a Mortgage Loan Officer resume truly stand out from the stack.

You're competing against other candidates who also have NMLS licenses, who also know loan products, who also claim strong sales skills. The difference-makers are in the details that show you understand the unique challenges and opportunities of this role.

Every hiring manager's nightmare is bringing on a loan officer who generates compliance violations.

Your resume should subtly but clearly communicate that you're not that person. Weave compliance awareness throughout your resume - mention your clean NMLS record, highlight any compliance training you've completed, and when describing achievements, include phrases like "while maintaining 100% compliance with federal lending regulations."

If you've never had a loan kicked back for compliance issues, that's worth mentioning.

❌ Don't ignore compliance considerations:

Originated high volume of loans with strong sales performance

✅ Do integrate compliance awareness:

Originated $18M in loans annually while maintaining perfect compliance record

with zero HMDA violations or fair lending concerns over 3-year period

Mortgage lending is inherently local, even when working for national lenders. Demonstrate your understanding of your specific market - mention your knowledge of local down payment assistance programs, your relationships with regional real estate brokerages, or your expertise with unique aspects of your market (like co-ops in New York, or agricultural properties in rural areas).

This shows you bring more than just general lending knowledge - you bring local market intelligence that takes years to develop.

Unlike many sales roles where leads come from marketing or cold outreach, successful Mortgage Loan Officers build their business through referral partnerships. Your resume should tell the story of how you develop and maintain these crucial relationships. Include specific examples - "Established preferred lender status with three top-producing real estate teams" or "Created monthly first-time homebuyer workshops that generated 25% of annual loan volume."

These specifics show you understand that sustainable success in mortgage lending comes from being a trusted advisor, not just a salesperson.

The mortgage industry is experiencing rapid technological change, from digital applications to automated verification systems.

Show that you're not just comfortable with technology, but that you actively leverage it to improve the borrower experience. Mention your use of digital tools like mobile loan applications, e-signatures, or video consultations. If you've maintained strong production during the shift to remote work, that's particularly relevant. This demonstrates adaptability that's crucial in today's evolving mortgage landscape.

Remember, your resume is often your first interaction with a potential employer in an industry built on trust and relationships. Every element should reinforce that you're not just qualified on paper, but that you understand the nuanced realities of originating mortgages in today's complex lending environment.

The goal isn't just to list your experience - it's to tell the story of a loan officer who generates volume while maintaining compliance, who builds lasting professional relationships, and who guides borrowers through one of the biggest financial decisions of their lives.

The mortgage industry has evolved significantly since the 2008 financial crisis, with stricter regulations like the SAFE Act requiring specific educational credentials. Your education section isn't just a formality - it's proof that you're legally qualified to originate loans and that you possess the foundational knowledge to navigate an increasingly complex regulatory landscape.

For Mortgage Loan Officers, education extends beyond traditional degrees.

You'll need to showcase your NMLS (Nationwide Multistate Licensing System) education, which includes 20 hours of pre-licensing education covering federal law, ethics, and lending standards. This isn't optional - it's the ticket to your career. List these certifications prominently, including your NMLS number once obtained.

While a bachelor's degree isn't always mandatory, having one in finance, economics, business administration, or accounting gives you a competitive edge. Community banks might be flexible, but larger institutions often filter candidates without degrees.

The key is presenting your education in a way that demonstrates both compliance and competence.

Start with your highest level of formal education, then add your mortgage-specific certifications. Include completion dates for NMLS courses - this shows you're current with regulations.

If you're transitioning from real estate, banking, or insurance, highlight relevant coursework that translates to mortgage lending.

❌ Don't write vaguely about your qualifications:

Bachelor's Degree - State University

NMLS Licensed

Some mortgage training courses

✅ Do provide specific, compliance-focused details:

Bachelor of Science in Finance - State University, 2021

GPA: 3.6/4.0 | Relevant Coursework: Real Estate Finance, Risk Management, Financial Markets

NMLS License #1234567 - Active in CA, NV, AZ (2023)

• 20-Hour SAFE Pre-Licensing Education - ABC Training Institute (March 2023)

• 8-Hour Annual Continuing Education - XYZ Academy (January 2024)

• FHA/VA Loan Processing Certification - Housing Finance Agency (2023)

Different states have varying requirements beyond federal minimums. California requires additional education on state-specific laws, while Texas has unique homestead regulations you'll need to understand.

If you're licensed in multiple states, list them clearly - this versatility is valuable to employers operating across state lines.

The mortgage industry rewards continuous learning. Include any additional certifications like Certified Mortgage Planning Specialist (CMPS) or coursework in specialized areas like reverse mortgages or construction loans.

These show you're not just meeting minimum requirements but actively expanding your expertise to serve diverse client needs.

Unlike other sales roles where awards might focus purely on volume, mortgage lending recognition often balances production with quality metrics like customer satisfaction scores, loan quality ratings, and compliance excellence. Your awards section needs to reflect this multifaceted nature of success in mortgage origination.

Production awards are the most common - President's Club, Top Producer, Million Dollar Club - but context is everything. A "Top 10% Producer" award at Wells Fargo carries different weight than the same achievement at a local credit union.

Specify loan volume in dollars rather than just units, as this demonstrates your ability to handle complex, high-value transactions.

Quality and compliance awards are increasingly valuable post-Dodd-Frank. Recognition for lowest default rates, highest customer satisfaction scores, or perfect compliance audits shows you're not just closing loans - you're closing the right loans. These awards reassure employers that you won't create regulatory headaches while chasing numbers.

❌ Don't list awards without context:

Top Producer - 2023

Customer Service Award

Best Team Player

✅ Do provide specific, quantifiable achievements:

President's Club Award - ABC Mortgage Corporation (2023)

• Top 5% nationally with $42M in funded loans across 156 transactions

• Maintained 0% early payment default rate and 98% customer satisfaction score

Excellence in FHA Lending Award - Regional Housing Authority (2022)

• Recognized for helping 47 first-time homebuyers achieve homeownership

• Specialized in down payment assistance programs with 100% compliance rate

Publications in mortgage lending might include articles in industry journals like National Mortgage News or Mortgage Professional America, blog posts on company websites about market trends, or contributions to local real estate publications. These demonstrate your market expertise and ability to educate clients - crucial skills when explaining complex loan products.

If you've written guides on topics like "Navigating VA Loans" or "Understanding Debt-to-Income Ratios," include them. These show you can break down complex concepts for clients. Speaking engagements at real estate offices or first-time homebuyer seminars also belong here - they prove your role as a trusted advisor in your community.

Create a separate "Awards & Recognition" section if you have three or more significant achievements.

Otherwise, integrate them into your experience section where they provide context for your accomplishments. Recent awards (within three years) are most relevant, unless older awards are particularly prestigious or from well-known institutions.

Remember that in mortgage lending, consistency matters as much as peaks. An award for "Five Years Consecutive President's Club" tells a better story than a single spectacular year.

It shows you can maintain performance through different market cycles - a valuable trait given the mortgage industry's sensitivity to interest rate changes.

The mortgage industry's interconnected nature means your reputation travels fast.

A reference from a respected real estate broker can open doors at multiple lenders, while a negative reference can close them just as quickly. Your references aren't just confirming employment - they're vouching for your ability to handle people's largest financial transactions with integrity and competence.

Your ideal references understand what makes a successful Mortgage Loan Officer. A branch manager who can speak to your production numbers, pull-through rates, and compliance record provides more value than a generic "hard worker" recommendation. Processing managers can attest to your application quality and attention to detail.

Underwriters (if you have good relationships) can confirm your ability to structure deals correctly the first time.

Real estate agent references require careful consideration. Choose established agents who've sent you multiple referrals over time, not just someone from a single transaction. Their endorsement carries weight because it represents repeated trust with their clients' financing. Similarly, builder representatives or financial advisors who've referred business demonstrate your ability to maintain professional partnerships.

❌ Don't list references without context:

References:

John Smith - 555-1234

Jane Doe - 555-5678

Bob Johnson - 555-9012

✅ Do provide references with clear professional relationships:

Professional References:

Sarah Martinez - Regional Sales Manager, First National Mortgage

Phone: 555-1234 | Email: [email protected]

Relationship: Direct supervisor for 3 years; can attest to $150M production volume

and consistent President's Club achievement

Michael Chen - Managing Broker, Premier Realty Group

Phone: 555-5678 | Email: [email protected]

Relationship: Primary referral partner; 50+ successful transactions together;

can speak to client service and communication skills

Mortgage lending often involves non-compete agreements and client confidentiality issues that complicate references.

If you're currently employed, you might not want your manager contacted immediately. Create a separate reference sheet noting "References available upon request - currently employed and conducting confidential search." This is standard in the industry and won't raise red flags.

When listing references from previous employers, be mindful of any non-solicitation agreements. A former colleague now at a different company might be a safer reference than someone still at your previous firm if there are competitive concerns. Always inform your references about potential calls and brief them on the position you're seeking - they should know if you're moving from retail to wholesale or shifting to a different market segment.

Different markets have varying reference expectations.

In the UK, employers often require written references on company letterhead. Australian employers might check your credit as part of their reference process. In Canada, privacy laws affect what previous employers can disclose. In the USA, some states have specific regulations about what employers can say about former employees.

Include at least one reference who can verify your licensing status and continuing education compliance. This might be a compliance officer or training coordinator.

Given the regulatory scrutiny in mortgage lending, having someone who can confirm your clean compliance record is invaluable.

Keep your reference list updated quarterly - production numbers change, people change positions, and contact information becomes outdated. After each successful placement, update your references on your new role and thank them for their support.

This maintains relationships for future opportunities.

Create different reference lists for different opportunities. Applying to a reverse mortgage specialist position? Include references who can speak to your experience with senior clients. Pursuing a construction lending role? Builder and contractor references become more relevant. This targeted approach shows strategic thinking and network depth.

Finally, remember that in mortgage lending, your references often become your future business partners. The manager who gives you a glowing reference today might become your wholesale account executive tomorrow. Treat every professional relationship as a long-term investment in your career network.

The mortgage industry's relationship-driven nature makes cover letters particularly crucial. Hiring managers want to see that you understand the delicate balance between sales targets and fiduciary responsibility.

They're looking for someone who can build referral networks with real estate agents while maintaining compliance standards that protect both borrowers and the institution.

Skip the generic "I'm writing to apply" opening.

Instead, lead with a specific achievement that demonstrates your understanding of current market challenges. Maybe you maintained loan volume during rising rate environments by pivoting to ARM products, or you built a thriving first-time homebuyer practice using state bond programs. Your opening should immediately signal that you understand the mortgage business beyond just taking applications.

❌ Don't open with generic enthusiasm:

Dear Hiring Manager,

I am excited to apply for the Mortgage Loan Officer position at your company.

I have been working in sales for five years and think I would be a great fit.

✅ Do lead with specific, relevant achievements:

Dear Ms. Johnson,

When interest rates jumped to 7% last year, I helped 73 families still achieve

homeownership by leveraging creative financing solutions including 2-1 buydowns

and state housing finance programs - maintaining my $3M monthly production target

while competitors saw 40% volume drops.

The mortgage industry constantly evolves - from TRID implementation to COVID-era forbearance programs to recent NAR settlement changes affecting buyer representation. Use your cover letter to show you're not just aware of these changes but have successfully adapted to them.

Mention specific programs you've mastered like FHA 203(k) renovation loans or USDA rural development loans if they're relevant to the employer's market.

Address the employer's specific market position. If they're a direct lender, emphasize your ability to sell in-house products. If they're a broker, highlight your relationships with multiple wholesale lenders. For credit unions, stress your member-service philosophy. This customization shows you understand their business model, not just the generic role of loan origination.

Mortgage lending success depends heavily on referral partnerships.

Describe how you've built relationships with real estate agents, financial planners, or builders. But balance this with compliance awareness - mention your clean audit record or your commitment to fair lending practices. Post-2008, employers need to know you can produce without creating regulatory risk.

Include specific examples of complex scenarios you've navigated - perhaps helping self-employed borrowers document income or structuring loans for investment properties. These examples demonstrate problem-solving abilities that go beyond basic order-taking.

End with specificity about what you bring to their team. If they're expanding into reverse mortgages and you have HECM experience, mention it. If they're growing their Hispanic market presence and you're bilingual, emphasize this alignment. Propose a concrete next step beyond "I look forward to hearing from you."

Remember that in mortgage lending, timing matters. Mention your current pipeline status and potential transfer timeline if you're currently originating. This shows professionalism and helps set realistic expectations about your availability while respecting any non-compete agreements you might have.

After diving deep into the intricacies of crafting a compelling Mortgage Loan Officer resume, here are the essential points to remember as you build yours:

Creating a standout Mortgage Loan Officer resume doesn't have to be overwhelming. With Resumonk, you can build a professional, polished resume that incorporates all these crucial elements while maintaining clean, readable formatting that hiring managers expect. Our AI-powered suggestions help you craft achievement-focused bullet points that showcase your loan origination success, while our professionally designed templates ensure your NMLS credentials, production metrics, and compliance achievements are presented with the prominence they deserve. Whether you're transitioning from processing, moving between lenders, or advancing your career in mortgage origination, Resumonk's tools are specifically designed to help financial services professionals like you tell their story effectively.

Ready to create your standout Mortgage Loan Officer resume?

Join hundreds of mortgage professionals who've successfully advanced their careers with Resumonk's intelligent resume builder. Our specialized templates and industry-specific recommendations will help you craft a resume that speaks directly to hiring managers in the mortgage industry.

Start Building Your Mortgage Loan Officer Resume →